Longevity Risk: Planning for a Longer Retirement

Increasing life expectancies present both opportunities and challenges for retirement planning in the contemporary world. Longevity risk, the risk of outliving your retirement savings, is a significant concern for many individuals. Planning for a longer retirement period is essential for ensuring a secure and comfortable retirement. In this article, we will examine the concept of longevity risk, its implications, and practical planning and management strategies for this risk.

Understanding Longevity Risk

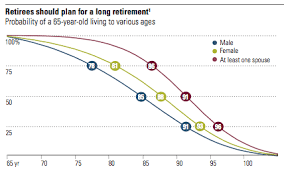

Longevity risk is the possibility that individuals will live longer than anticipated, resulting in the depletion of retirement savings and financial insecurity in old age. Despite the fact that longer lifespans are generally viewed as a positive development, they necessitate careful retirement planning. Failure to account for this risk may result in financial difficulties and an inability to meet future requirements.

The Consequences of Longevity Risk:

Longevity risk poses several implications for retirement planning:

1. Increased Retirement Expenses:

Longer lifespans translate into more years spent in retirement, resulting in an increase in expenses. Medical costs, long-term care expenses, and maintaining a desired lifestyle over an extended period can put a strain on retirement savings. Inability to account for these additional costs can result in financial strain in later years.

2. Inadequate Retirement Savings:

Underestimating the duration of retirement can lead to insufficient savings. If you plan for a shorter retirement period and then outlive your expectations, you run the risk of outliving your savings. It is essential to have a realistic estimation of your lifespan to ensure that your retirement savings will last throughout your retirement years.

3. Impact on Retirement Income:

Longevity risk can have a substantial effect on retirement income. If you deplete your savings sooner than expected, you may be forced to rely solely on Social Security or other sources of fixed income. This may result in a lower standard of living and limited financial flexibility.

Planning and Managing Longevity Risk Strategies:

1. Start Saving Early:

One of the most effective strategies for mitigating longevity risk is to begin saving as early as possible for retirement. The power of compounding allows your savings to grow over time, resulting in a larger nest egg that can support a longer retirement. Small contributions made consistently can make a substantial difference over time.

2. Create a Realistic Retirement Budget:

Create a retirement budget that takes into account both mandatory and optional expenses. Consider costs associated with healthcare, housing, transportation, travel, and recreational activities. Be realistic about your desired lifestyle and ensure your retirement savings align with your budgetary needs.

3. Diversify Your Sources of Retirement Income:

Relying solely on a single source of retirement income, such as Social Security, is risky. Diversify your income streams by including pensions, annuities, rental income, and dividend-paying investments, among others. This diversification can contribute to a stable and sustainable retirement income stream.

4. Take into Account Longevity Insurance and Deferred Annuities:

Longevity insurance and deferred annuities are financial products designed to mitigate the risk associated with aging. These products provide a stream of guaranteed income beginning at a predetermined age, which is typically older than the traditional retirement age. By including these options in your retirement plan, you can mitigate the risk of outliving your savings.

5. Review and Modify Investment Strategies:

Review and modify your investment strategies on a regular basis so that they align with your changing retirement goals and time horizon. Consider adopting a more conservative investment strategy as you age to safeguard your wealth. In order to ensure that your investment portfolio remains aligned with your changing needs and market conditions, it is essential to strike a balance between risk and reward.

6. Consider Long-Term Care Insurance:

In later years, long-term care expenses can be a significant financial burden. Consider purchasing long-term care insurance to reduce the likelihood that your savings will be depleted by medical expenses. Long-term care insurance may cover nursing home care, assisted living, and home healthcare.

7. Continuously Monitor and Reevaluate:

Continuously monitor and reevaluate your retirement plan and financial objectives. Ensure that your portfolio, income projections, and expenses remain on track by reviewing them. Make adjustments as needed to address any gaps or changes in your circumstances.

8. Cooperate with a Financial Advisor:

Working with a qualified financial advisor can provide valuable insights and direction for managing longevity risk. A financial advisor can assist you in navigating complex retirement planning decisions, assessing your risk tolerance, and developing a strategy tailored to your unique needs and objectives. More info about Pacific Wealth Management.

Conclusion:

Planning for a longer retirement is crucial for mitigating the potential risks associated with rising life expectancies. By understanding the implications of longevity risk and implementing strategies such as saving early, creating a realistic retirement budget, diversifying income sources, considering longevity insurance, reviewing investment strategies, obtaining long-term care insurance, continuously monitoring your plan, and consulting a financial advisor, you can increase your financial security and enjoy a comfortable retirement.

Remember that longevity risk necessitates ongoing monitoring and adjustment as you progress through the various stages of retirement. You can achieve financial peace of mind, maintain your desired lifestyle, and ensure a prosperous and fulfilling retirement journey by proactively addressing this risk.