Retirement Planning for Baby Boomers: Strategies for Late Career Professionals

Planning for retirement is an essential aspect of financial planning, particularly for baby boomers who are nearing the end of their careers. As a generation that has experienced substantial societal and economic changes, baby boomers face unique retirement challenges and opportunities. Retirement planning requires careful consideration of financial objectives, lifestyle expectations, and potential income sources. In this blog post, we will discuss retirement planning strategies that are tailored specifically to baby boomer professionals in their late careers.

- Assess Your Financial Readiness: Assessing your financial readiness is the first step in retirement planning. Start by assessing your current financial situation, including your savings, investments, and any retirement accounts you may have. Consider collaborating with a financial advisor or retirement planner who can assist you in assessing your financial resources, projecting your future income, and estimating your retirement expenses.

- Define Your Retirement Objectives: Clearly define your retirement objectives and goals. Consider factors such as where you wish to reside, how you intend to spend your time, and the type of lifestyle you seek. This will assist you in estimating the amount of money required to support your retirement lifestyle and setting a savings goal.

- Calculate Your Retirement Income Gap: After determining your retirement objectives, calculate the income gap between your anticipated retirement expenses and the income you can expect from sources such as Social Security, pensions, and other retirement accounts. This will help you determine how much additional retirement savings you need to accumulate.

- Maximize Your Retirement Contributions: Utilize retirement savings vehicles such as employer-sponsored 401(k) plans and Individual Retirement Accounts (IRAs) to maximize your retirement contributions. Consider contributing the maximum amount permitted by law to receive tax benefits and employer contributions. You may be eligible for catch-up contributions as you approach retirement, allowing you to contribute additional funds to your retirement accounts.

- Diversify Your Investments: Ensure that your investment portfolio is properly diversified in order to minimize risk and maximize returns. Consider a variety of asset classes, including stocks, bonds, real estate, and other investment vehicles, such as stocks, bonds, and real estate. Diversification protects your investments from market volatility and improves your chances of reaching your long-term financial objectives.

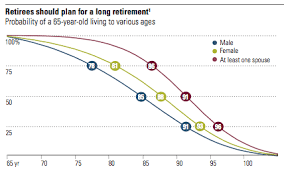

- Consider Delaying Social Security Benefits: Baby boomers have the option of delaying Social Security benefits past the eligibility age. By delaying benefits, you can increase the monthly payout when benefits are eventually received. This strategy can be especially advantageous for those who have other sources of income and can afford to wait.

- Consider the Costs of Healthcare and Long-Term Care: When planning for retirement, it is essential to evaluate the costs of healthcare and long-term care. Include Medicare, supplemental insurance, and long-term care insurance in your research and evaluation of available health insurance options. Understanding these costs will assist you in budgeting appropriately and securing adequate coverage in retirement.

- Review and Modify Your Estate Plan: Regularly review your estate plan to ensure that it reflects your current wishes and financial situation. Update beneficiary designations, create or revise a will, and if necessary, consider establishing a trust. A consultation with an estate planning attorney can help you distribute your assets in accordance with your wishes and minimize potential tax implications.

- Explore Opportunities for Part-Time Work or Consulting: If you are not yet ready for full retirement, consider exploring opportunities for part-time work or consulting that align with your skills and interests. This can provide a sense of purpose and engagement while supplementing your retirement income. It may also enable you to postpone withdrawals from your retirement accounts, giving them additional time to grow.

- Develop a Sustainable Withdrawal Plan: Create a withdrawal strategy that will ensure the longevity of your retirement funds. Consider your life expectancy, anticipated investment returns, inflation, and any required minimum distributions (RMDs) from retirement accounts. What does Financial Advisor do? Consult a financial advisor to develop a plan that strikes a balance between your income requirements and the maintenance of your savings.

- Seek Professional Financial Guidance: Planning for retirement can be complicated, especially for late-career professionals with unique financial circumstances. Consider working with a retirement planning-focused financial advisor. A financial advisor can help you navigate the complexities of retirement planning, create a personalized plan, and provide ongoing guidance to ensure you remain on track to achieve your financial objectives.

- Stay Informed and Flexible: Remain up-to-date on changes to tax laws, Social Security regulations, and retirement planning strategies. Attend retirement planning-related seminars, workshops, or webinars to stay abreast of the most recent trends and insights. Be willing to adapt your retirement plan to changing circumstances or market conditions as necessary.

In conclusion, planning for retirement for baby boomers necessitates a comprehensive approach that takes individual objectives, financial resources, and lifestyle expectations into account. Late-career professionals can benefit from a variety of retirement planning strategies, including maximization of retirement contributions, diversification of investments, and evaluation of healthcare costs. Baby boomers can navigate the complexities of retirement planning and work towards a financially secure and fulfilling retirement by seeking professional financial planning advice and keeping abreast of trends in retirement planning. It is never too late to begin planning for your retirement, so take the necessary steps to secure your financial future immediately.